具体描述

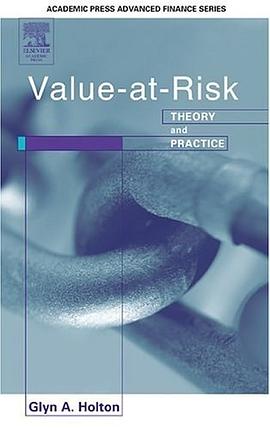

Value-at-risk (VaR) is a measure of market risk that has been widely adopted since the mid-1990s for use on trading floors. This is the first advanced book published on VaR. It describes how to design, implement, and use scalable production VaR measures on actual trading floors. It takes readers from the basics of VaR to the most advanced techniques, many of which have never been published in book form.

Practical, detailed examples are drawn from markets around the world, including: Euro deposits, Pacific Basin equities, physical coffees, and North American natural gas.

Real-world challenges relating to market data, portfolio mappings, multicollinearity, and intra-horizon events are addressed in detail. Exercises reinforce concepts and walk readers step-by-step through computations.

Sophisticated techniques are fully disclosed, including: quadratic ("delta-gamma") methods for nonlinear portfolios, variance reduction (control variates and stratified sampling) for Monte Carlo VaR measures, principal component remappings, techniques to "fix" estimated covariance matrices that are not positive-definite, the Cornish-Fisher expansion, and orthogonal GARCH.

* First advanced text on Value-at-Risk

* Practical, detailed examples drawn from markets around the world

* Exercises reinforce concepts and walk readers step-by-step through computations

作者简介

目录信息

读后感

评分

评分

评分

评分

用户评价

初次翻阅《Value-at-Risk》,我怀揣着一丝好奇,更多的是期待。市面上关于金融风险的书籍琳琅满目,但真正能打动我,让我愿意花费时间和精力去深入理解的却屈指可数。这本书从一开始就以其独特的叙事方式吸引了我,它不是枯燥的教科书,而更像是一场与作者思想的深度对话。作者以一种旁观者清的视角,剖析了金融市场运作的内在逻辑,以及风险是如何在这种逻辑中扮演至关重要的角色。我尤其被书中对“风险偏好”和“风险承受能力”的探讨所吸引。这不仅仅是理论上的概念,更是关乎到每一家金融机构生存与发展的根本问题。书中提出的“风险画像”概念,让我眼前一亮,它帮助我理解如何将一家机构的风险特征进行可视化,从而更直观地进行评估和管理。我发现,作者在阐述某些概念时,非常注重逻辑的严谨性和层层递进的清晰度。例如,在讲解不同风险度量方法时,作者会先介绍其基本原理,然后逐步深入其数学模型,再结合实际应用场景进行分析,这种由浅入深的学习过程,极大地降低了理解的难度,也让我在潜移默化中掌握了这些复杂的知识。更难能可贵的是,书中并没有回避金融市场中的不确定性,而是积极倡导一种“拥抱不确定性”的风险管理哲学,这是一种非常成熟和前瞻性的观点,也让我对未来的金融风险管理有了更深的思考。

评分作为一名在金融领域摸爬滚打多年的老兵,阅读《Value-at-Risk》这本书,无疑是一次对我过往经验的一次系统性梳理和升华。我一直在寻找一本能够真正触及风险管理核心,并且能将复杂的理论与实际应用无缝衔接的书籍,而这本书给我的感受,绝不仅仅是“找到了”,更是一种“原来如此”的豁然开朗。它没有那些空泛的理论堆砌,也没有那些令人望而生畏的数学公式,而是以一种极其人性化的视角,带领我一步步走进风险的真实世界。书中对风险的定义、分类、度量和管理,都显得那么贴切而深刻。作者通过大量真实的案例分析,将抽象的风险概念具象化,让我能够清晰地看到风险是如何在市场波动中滋生、蔓延,并最终对机构的生存构成威胁。尤其令我印象深刻的是,书中对于不同类型风险的区分和量化方法,例如市场风险、信用风险、操作风险等,都给出了详细的阐述和具体的实践指导。我特别欣赏作者在处理“尾部风险”和“黑天鹅事件”时所展现出的审慎态度,这与当前金融市场频繁出现的极端事件不谋而合,也促使我反思了过去在风险评估中可能存在的盲点。这本书不仅仅是理论上的指南,更是一套实操性的工具箱,为我提供了应对复杂金融挑战的全新思路和方法。它让我认识到,风险管理并非一成不变的教条,而是一个需要持续学习、不断调整和灵活应变的动态过程。每一次阅读,都能从中获得新的启发,也让我对自身的风险管理能力有了更深入的认识和提升。

评分《Value-at-Risk》这本书,对我来说,是一次对金融风险认知的“颠覆”。作者以一种极其严谨而又不失幽默的笔触,深入剖析了金融市场中风险的无处不在,以及理解和管理风险对于金融机构生存和发展的重要性。我一直认为,风险管理是一种“减法”,目标是尽可能地消除风险。然而,这本书却让我看到了风险的另一面:它是一种“加法”,是实现更高收益的必要条件。作者通过对“风险-收益权衡”的深刻论述,阐释了如何在可接受的风险水平下,最大化机构的价值。我尤其喜欢书中关于“风险定价”的探讨。这部分内容,让我看到了风险是如何被纳入到资产定价过程中,并影响着市场参与者的决策。作者强调,有效的风险管理需要高度的专业性和持续的学习能力,因为金融市场和风险形式都在不断变化。书中对“监管合规”和“风险文化”的并重,也让我看到了风险管理在现代金融机构中的地位。它不仅仅是业务部门的责任,更是需要整个机构共同承担的使命。此外,书中对“压力测试”和“情景分析”的详细阐述,也为我提供了应对极端市场事件的有力工具。这本书,让我学会了如何以一种更积极、更主动的态度去拥抱风险,并将其转化为提升机构竞争力的源泉。

评分《Value-at-Risk》这本书,可以说是一次对金融风险认知的“重塑”。我一直认为,金融风险是一种客观存在,是可以被量化和预测的。然而,这本书却让我认识到,风险的本质是复杂的、动态的,并且充满了不确定性。作者以一种非常哲学化的方式,探讨了风险的起源、发展以及对金融体系的影响。我尤其被书中对“认知偏差”和“行为金融”在风险决策中的作用的分析所吸引。这部分内容,让我意识到,人类自身的心理因素,往往会放大或扭曲我们对风险的判断,从而导致错误的决策。书中提出的“反脆弱”概念,更是让我耳目一新。它不仅仅是关于如何规避风险,更是关于如何从风险和混乱中变得更强大。这种积极的风险管理哲学,与我以往的认知截然不同,也为我打开了新的视野。我欣赏作者在论述过程中,能够将宏观的理论与微观的实践相结合,使得读者既能理解风险管理的大方向,又能掌握具体的执行方法。例如,在介绍“风险隔离”时,作者不仅解释了其理论基础,还提供了多种实际操作的案例,让我能够学以致用。这本书,让我明白,风险管理并非一种技术,而是一种艺术,需要经验、洞察力和智慧的结合。

评分我必须说,《Value-at-Risk》这本书,彻底改变了我对风险管理的传统认知。过往,我总觉得风险管理是一件非常“苦差事”,充满了繁琐的计算和无休止的报告。然而,这本书的出现,让我看到了风险管理更积极、更具建设性的一面。作者将风险视为一种机会,一种可以被理解、被控制、甚至被利用的内在驱动力。书中对于“风险-收益权衡”的深刻洞察,让我看到了风险管理不仅仅是“规避风险”,更是一种“优化风险”的过程。我特别欣赏书中关于“情景分析”和“压力测试”的论述,这部分内容提供了非常实用的工具,让我能够模拟各种极端市场条件下机构的反应,从而更好地制定应对策略。作者并没有将这些工具描绘成万能药,而是强调它们在实际应用中的局限性和需要注意的细节,这种真实和坦诚,让我对书中的内容更加信服。此外,书中对“数据质量”和“模型风险”的警示,也给我留下了深刻的印象。它提醒我,任何风险管理方法,其有效性都高度依赖于输入数据的准确性和模型的合理性。这种对细节的关注,正是优秀风险管理所不可或缺的。阅读这本书,就像是为我打开了一扇全新的窗户,让我能够从更宏观、更战略的层面去审视风险,并将其融入到机构的整体发展战略之中。

评分《Value-at-Risk》这本书,对我来说,是一次深刻的金融启蒙。作者以一种极其清晰且富有逻辑性的方式,为我揭示了金融市场运作的内在逻辑,以及风险在这个体系中所扮演的关键角色。我一直认为,风险管理的核心在于“量化”,即用精确的数字来衡量风险。然而,这本书却让我认识到,量化只是风险管理的一部分,更重要的是对风险的“理解”和“管理”。作者通过对历史上多次金融危机的案例分析,生动地展示了风险是如何在看似稳定的市场中孕育,并最终对金融体系造成颠覆性的影响。我尤其喜欢书中关于“风险文化”的论述。作者强调,再先进的风险管理模型,如果没有与之匹配的风险文化,都将形同虚设。这种对“软性”因素的重视,让我看到了风险管理更深层次的内涵。书中对“风险偏好”和“风险承受能力”的探讨,也让我看到了风险管理如何与机构的战略目标相协调。它不仅仅是规避风险,更是要找到一个最优的风险水平,以实现可持续的增长。此外,书中对“信息不对称”和“道德风险”的深入分析,也让我看到了风险管理在信息传递和激励机制设计方面的应用。这本书,让我学会了如何以一种更全面、更系统的方式去理解和管理风险,并将其转化为提升机构韧性和竞争力的关键要素。

评分《Value-at-Risk》这本书,对我而言,更像是一次与金融世界内心对话的旅程。作者没有用高深的术语堆砌,而是以一种极其平实且富有洞察力的语言,带领我深入理解风险的本质。我一直认为,风险管理的核心在于“理解”二字。只有真正理解了风险的来源、性质和潜在影响,才能有效地进行管理。这本书,恰恰满足了我对“理解”的渴望。作者通过对历史上的金融危机案例的深入剖析,揭示了风险是如何在看似平静的市场中孕育,并最终爆发的。我尤其被书中对“风险胃纳”和“风险限额”的探讨所吸引。这部分内容,让我看到了风险管理如何在具体的操作层面落地,并为机构的经营活动提供有效的指引。作者强调,风险管理并非孤立的部门职责,而是需要融入到机构的每一个业务环节中,形成一种全员参与的风险文化。这种系统性的思维方式,让我对风险管理有了更全面的认识。此外,书中对“模型风险”的警示,也让我深刻意识到,任何模型都只是对现实的一种近似,其有效性会随着时间和市场环境的变化而衰减,需要持续的检验和更新。这本书,让我学会了如何以一种更谦卑、更审慎的态度去面对风险,并将其转化为提升机构韧性的契机。

评分阅读《Value-at-Risk》,给我带来的不仅是知识的增长,更是一种思维方式的转变。过去,我常常将风险视为洪水猛兽,一心想着如何将其彻底规避。然而,这本书却让我看到了风险的另一面:它是一种驱动力,是实现目标过程中不可或缺的一部分。作者以一种非常细腻的笔触,剖析了风险与收益之间的微妙关系,并提出了“风险优化”的理念,即如何在可接受的风险水平下,最大化收益。我尤其喜欢书中关于“风险母语”的阐述。作者认为,风险管理需要一种共通的语言,一种能够让所有参与者都理解和认同的风险沟通方式。这对于建立有效的风险文化至关重要。书中对“风险分散”和“风险集中”的比较分析,也让我受益匪浅。它让我认识到,不同的风险管理策略,需要根据具体的业务模式和市场环境进行选择,不存在放之四海而皆准的通用法则。作者在强调理论的同时,也非常注重实践的指导性,书中提供的各种量化工具和分析方法,都具有很强的可操作性,让我能够直接应用于日常工作中。这本书,让我学会了如何与风险共舞,如何在不确定性中寻找确定性,从而更好地实现机构的战略目标。

评分在我看来,《Value-at-Risk》不仅仅是一本金融书籍,更是一部关于金融智慧的启迪录。作者以其深厚的学识和敏锐的洞察力,为我揭示了金融市场运作的深层逻辑,以及风险在这个体系中所扮演的关键角色。书中对于“风险文化”的强调,更是点睛之笔。它让我明白,再先进的风险管理模型,如果没有良好的风险文化作为支撑,都将是空中楼阁。作者通过大量的案例,生动地展现了风险文化对机构绩效的影响,这种影响是潜移默化的,却又是决定性的。我尤其喜欢书中对“风险的沟通与披露”的论述。作者强调了清晰、准确、及时的信息披露对于建立市场信任和有效管理风险的重要性。这与当前金融监管的趋势高度契合,也让我对如何更好地与投资者和监管机构沟通风险有了更清晰的认识。书中对“内控”与“风控”关系的阐述,也给我留下了深刻的印象。它指出,有效的风险管理需要与健全的内部控制体系相互配合,形成一个有机整体。这种系统性的思维方式,让我能够更全面地理解风险管理的内涵。读完这本书,我不仅对风险有了更深的理解,更重要的是,我学会了如何以一种更积极、更主动的态度去拥抱风险,并将其转化为提升机构竞争力的动力。

评分当我翻开《Value-at-Risk》这本书时,我并没有预料到它会对我产生如此大的影响。过往,我总是习惯于用静态的眼光看待风险,认为只要将风险量化到位,就能万事大吉。然而,这本书却让我认识到,风险是一个动态演化的过程,需要持续的监控和调整。作者以一种非常生动的方式,描绘了金融市场中的风险涟漪效应,以及风险是如何从一个点蔓延到整个体系的。我尤其欣赏书中关于“风险传导机制”的论述。这部分内容,帮助我理解了风险是如何在不同资产、不同市场之间进行传递的,从而更好地识别和管理风险敞口。作者并没有将风险管理描绘成一种纯粹的计算过程,而是强调了“人的因素”在其中扮演的重要角色。例如,在论述“道德风险”时,作者就深入分析了激励机制和行为模式对风险产生的影响。这种对人性弱点的洞察,让我对风险管理有了更深刻的理解。此外,书中对“数据可视化”和“风险报告”的强调,也让我看到了风险管理在信息传递方面的应用。清晰、简洁、具有说服力的风险报告,能够帮助管理层更好地做出决策。这本书,让我学会了如何以一种更动态、更具前瞻性的视角去审视风险,并将其转化为提升机构竞争力的利器。

评分写论文时用过

评分写论文时用过

评分写论文时用过

评分写论文时用过

评分写论文时用过

相关图书

本站所有内容均为互联网搜索引擎提供的公开搜索信息,本站不存储任何数据与内容,任何内容与数据均与本站无关,如有需要请联系相关搜索引擎包括但不限于百度,google,bing,sogou 等

© 2026 qciss.net All Rights Reserved. 小哈图书下载中心 版权所有